Metaverse Index Monthly Update - May 2021

May was a challenging month for the crypto markets. We certainly got our fair share of FUD between regulatory threats, Elon Musk tweets, China power outages, and liquidation cascades. The fear was apparent in the price action, with most crypto assets down significantly during the month. However, ETH and some DeFi tokens held up relatively well thanks to, dare I say, fundamentals. ETH is hitting all-time highs on many metrics of network activity, and it’s hard to bet against it heading into EIP-1559. As for DeFi, we continue to see strong cash flows despite market turmoil. Uniswap and Aave are bringing in more fees than the entirety of the Bitcoin network. Furthermore, the success of Polygon and the anticipation of L2 solutions going live are keeping many optimistic about the scalability of Ethereum and DeFi.

As we would expect in such an environment, The Metaverse Index (MVI) underperformed BTC and ETH. MVI declined by -45% in May, while BTC was down 35.4%, and ETH returned -2.5%. This is not surprising given the characteristics of the tokens in the MVI. Mostly mid and small caps, often at an earlier stage in their development relative to DeFi, these tokens carry higher risk and are expected to be more volatile on the downside as well as the upside. And while there are many claims that NFTs are dead, we would agree with Mason that the data tells a different story.

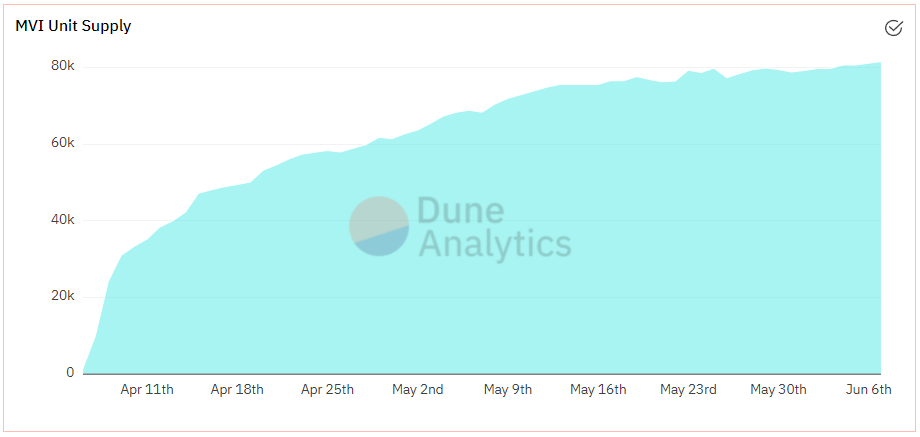

MVI unit supply continued to grow during May. Despite the market conditions and a reduction in liquidity mining incentives, we added around 20,000 new units this month. Retention rates are pretty strong, with 82.5% for the May cohort compared to 79.8% for the April cohort. With many Metaverse tokens down ~75% from ATH, despite unchanged or better fundamentals, this might be a good opportunity to start placing bets on the metaverse by picking up some MVI.

Looking at some early risk and performance metrics, MVI has done a good job balancing the performance of the underlying tokens and diversifying away some of the systemic risk. For example, in May, returns for the underlying tokens ranged between -34% and -64.4%, while MVI returned -45%. Performance numbers since inception tell a similar story.

On the risk side, since its inception, MVI has a standard deviation of 9.8% compared to 7.9% for ETH over the same period. The underlying tokens, however, displayed a standard deviation between 8.7% and 16.2%.

Overall, data shows that MVI, so far, has a stronger relationship with BTC and ETH than DPI, for example. Since its inception, MVI has a correlation of 0.76 and 0.83 to ETH and BTC, respectively. Its beta to ETH is also relatively high at 0.66. The upside and downside capture ratios also paint an interesting picture, with MVI capturing 173.9% of BTC’s upside and 151.8% of BTC’s downside. For ETH, the numbers are 74.6% and 124.8%, respectively.

Project Highlights

Turning our attention to the underlying tokens, we saw a sea of red in May, despite many positive developments. While fundamentals might seem irrelevant from time to time, we still wanted to highlight some of the projects in MVI and what they are up to.

The ‘least worst’ performer in May was WAXE, which saw a -34% drop during the month.

While updates from the team were fairly limited, there was a hint from The Block that WAX would provide the backend for eBay’s upcoming NFT marketplace. However, there is still no official confirmation from WAX or eBay as of the time of writing. There was a flurry of positive articles covering WAX more generally, though, including from Coindesk and, of course, our very own coverage on MetaPortal. These focused on the three main trends for WAX at the moment, namely explosive growth during 2021, partnerships with big brands, and the lower energy consumption of the WAX blockchain compared to Ethereum.

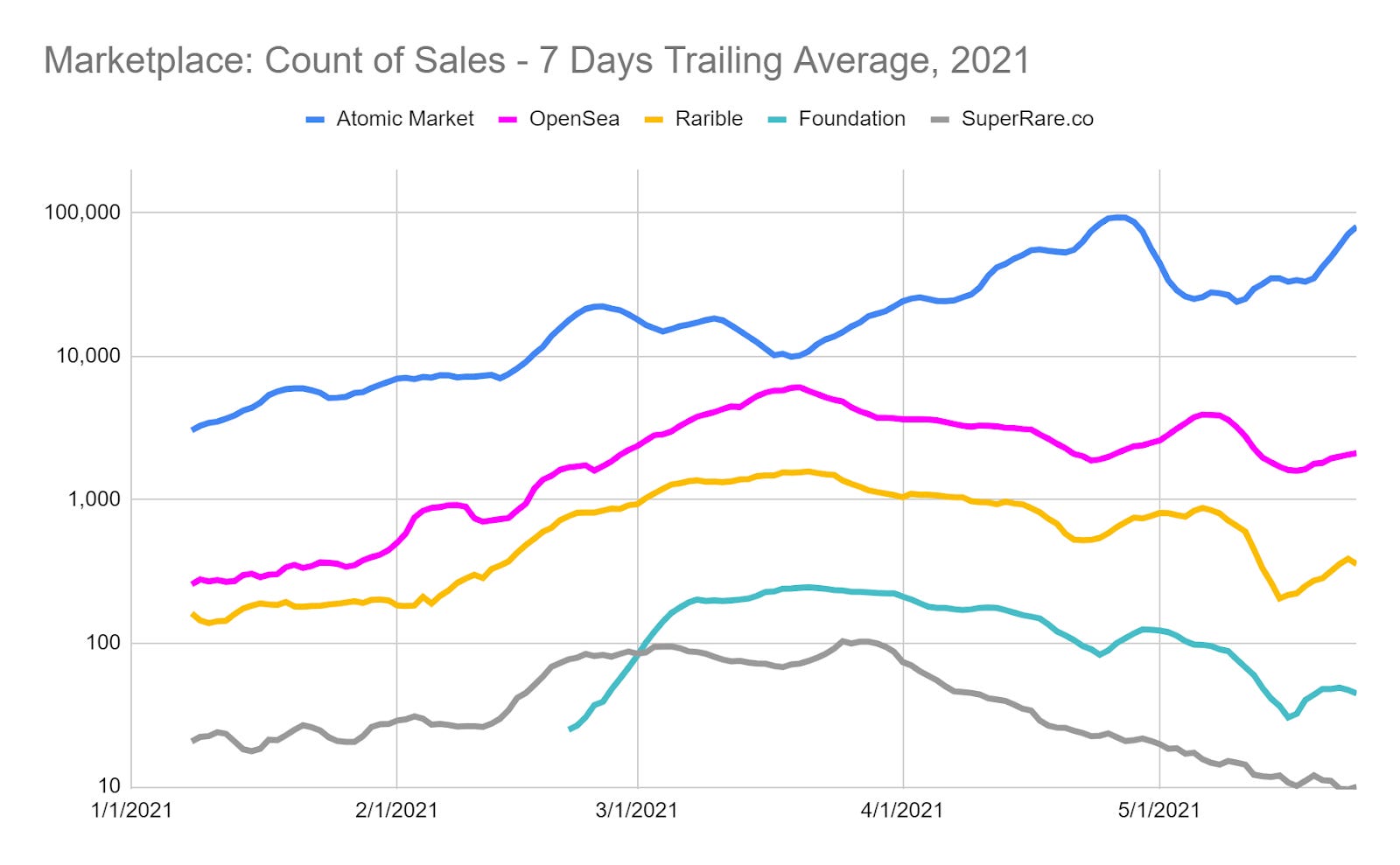

If we look at the numbers, despite the cooldown in crypto token prices and NFT sales, WAX/ETH LPs saw two highly profitable revenue distributions in May. A total of 230 ETH or $784,660 was distributed over the two 14 day epochs, showing that secondary market activity on WAX continued apace, even during market turmoil.

This was backed up by the data from DappRadar, shown above. Atomic Market (one of the most popular secondary markets for WAX NFTs) continues to lead in sales and even reached all-time highs again after the shaky start to May.

So with the stars aligning for WAX in terms of bullish news and 100% APR on the $10m LP pool for WAXE holders, there really wasn’t much of a reason to be selling last month, which seems to be reflected in the (relative) price action.

Another project that doesn’t get nearly enough attention is NFT20, powered by the MUSE token. It was founded by Jules and Adam with no external funding or presale, and the guys have been pretty vocal about building the right way. We think they are doing just that.

In May, the team deployed their NFT DEX on Polygon, doing so ahead of NFTX, and highlighted “some great organic usage” in their recent community update. They also completed a strategic token sale to diversify the Treasury, raising $750,000 in DAI from DeFiance Capital and Stake Capital. There have also been ongoing discussions about distributing fees to token holders. The conversation has continued over the last three months, with the latest proposal calling for the creation of an xMUSE token that will capture the fees from the protocol. The design is part Curve, part Sushi model with some of its own mechanics. While not final, we look forward to seeing how things play out on this front.

Not related directly to the monthly update, we wanted to highlight several other research pieces that we published in May. In the most recent article, we covered Sandbox and the $SAND token. Several weeks prior, we released a macro piece comparing traditional gaming business models and those of NFT games. We mentioned $SAND and $AXS, but the article applies more broadly to the NFT gaming sector.

Summary

Last week, we successfully rebalanced MVI in line with the methodology. Relative to portfolio allocations at the previous rebalance, we have increased exposure to SAND and WAXE while reducing positions in AXS, DG, and RFOX. These changes are mainly attributed to the liquidity dynamics, which were exacerbated by market volatility. SAND and WAXE maintained strong liquidity, while AXS, DG, and RFOX saw some deterioration in DEX liquidity. There were no new token additions in this month’s rebalance.